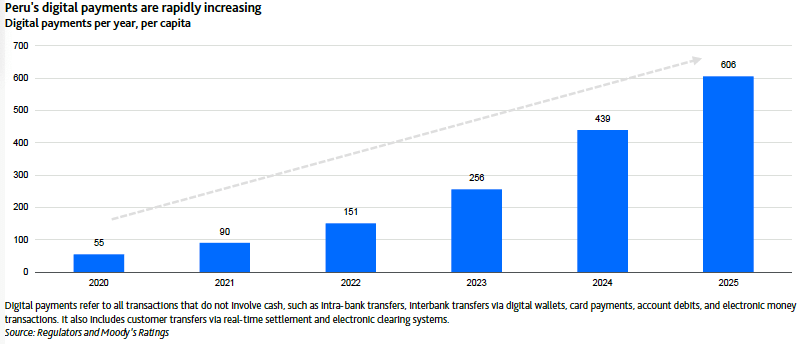

Peru, December 6, 2025 – The Central Reserve Bank of Peru (BCRP) published its updated rulebook for payments in the official gazette, strengthening its compliance framework and fostering transparency through data requirements, including new cyber-security rules, as the banking system rapidly accelerates digitalization of its operations. The new rules mandate that payment fees be nondiscriminatory, cost-based, and subject to an annual review by the regulators. The new rulebook is effective 1 April (replacing the 2010 version) and is credit positive for Peru’s financial system because it promotes competition, supporting the continued expansion of digital payments (see exhibit) and increased credit volumes by enhancing efficiencies across the banking sector.

Currently, low-value digital payments (less than PEN15,000 or $5,000) in Peru are largely controlled by banks, with interbank transfers comprising 66% of this total in the first half of 2025 (H1 2025), in accordance with data available in the BCRP’s September 2025 National Payments Systems Report. The updated rulebook will encourage new payment solutions and require interoperability among new systems, cementing the 2023 Payment Services Interoperability Regulation aimed mainly for digital wallets, enabling users to transfer funds regardless of provider or account type. This shift will initially reduce debit and credit card and current account revenue for Peru’s banks, which comprised on average about 8% of net revenues of the four largest banks as of September 2025. In addition, greater use of digital payments can drive growth in banking services, leading to larger deposit inflows and an expanded addressable market.

Instant payments accounted for 11% of low-value payments in H1 2025 and were dominated by two digital wallets: Yape, managed by the country’s largest bank Banco de Crédito del Perú (BCP, Baa1 stable, baa11), with 82% market share, and Plin, with 18%, a joint venture between next three largest banks in Peru, Banco BBVA Perú (Baa1 stable, baa2), Scotiabank Perú S.A.A. (Baa1 stable, baa2), and Banco Internacional del Perú S.A.A. (Baa1/Baa1 stable, baa2).

Competition for payments is poised to increase in Peru with the BCRP’s late 2026 planned introduction of its national digital payments platform, which is similar to Brazil’s PIX, Colombia’s Bre-B, or India’s UPI. However, Yape is already gearing up for competition, diversifying revenue streams beyond transaction fees, offering small installment loans and insurance brokerage, accelerating its path to the monetization of its client base. Payments are still the dominant contributor to Yape’s revenues, at 53%, followed by lending at 20%, as of September 2025.

As more customers adopt digital payments, electronic transactions through bank accounts increase. The shift allows banks to reduce their costs for cash transport and security – expenses that are particularly high in Peru, where many communities face limited access to financial services because of the country’s complex geography.

Credit Outlook: 15 December 2025. Pg. 14

Moody’s Investors Service