Australia, December 9, 2025 – Australian resources company BHP Group Limited (A1 stable) announced it has entered into a binding agreement with Global Infrastructure Partners (GIP), a part of BlackRock, regarding BHP’s share of the Western Australia Iron Ore (WAIO) inland power network. Under the agreement, a trust entity will be established, 51% owned and controlled by BHP, with GIP providing $2 billion in funding for a 49% minority stake. BHP will pay the entity a tariff linked to its share of WAIO’s inland power over a 25-year period. Importantly, BHP retains full operational control of WAIO and its inland power infrastructure, and the agreement does not affect existing joint venture arrangements or asset ownership.

BHP announced that the net proceeds will be incorporated into and evaluated in accordance with its capital allocation framework.

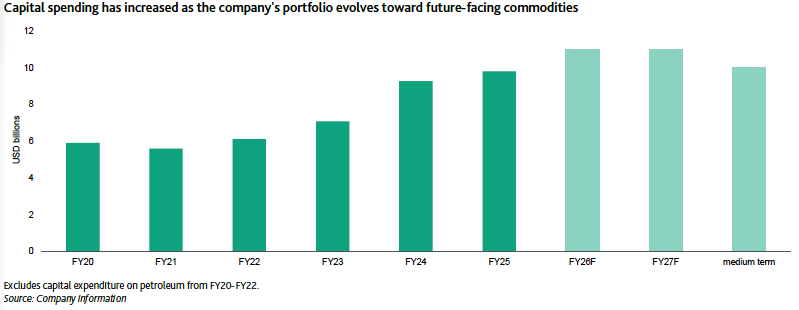

We expect the proceeds from the minority stake sale to increase liquidity and support the high capital spending requirements of the company in the medium term. BHP’s capital spending has increased as the company’s portfolio evolves toward future-facing commodities such as copper and potash. The company expects capital and exploration spending of around $11 billion annually in fiscal 2026 (ending June 2026) and fiscal 2027, with a planned reduction to around $10 billion a year on average from fiscal 2028 through to fiscal 2030 (see exhibit).

We regard the minority stake sale as equity in nature. Our understanding is that there is no mechanism for GIP to achieve preset target returns.

It is our expectation that BHP will fully consolidate the trust entity and that the cash outflow related to the tariff payments will represent less than 1% of the overall group’s earnings. Given BHP’s robust earnings generation capacity, these payments are immaterial and are not expected to have a meaningful impact on the group’s credit metrics or overall credit quality. We expect BHP’s track record of conservative credit metrics, excellent liquidity position, clearly articulated financial policies and flexible dividends to support its current growth phase while retaining credit metrics in line with our parameters for its ratings.

Credit Outlook: 15 December 2025. Pg. 10

Moody’s Investors Service

You must be logged in to post a comment.