Air passenger demand will remain severely depressed in 2021, will not see a substantial recovery before 2023. Health concerns, changes in corporate travel policies, potential restrictions on international arrivals, and lower discretionary spending because of weaker GDP and higher unemployment will constrain air passenger demand into 2022. Demand in 2023 could approach that of 2019, but the uncertain timing of the coronavirus receding on a more permanent basis makes forecasting a challenge.

Many airlines have improved liquidity, but at the cost of rising debt burdens. Stronger and state-supported airlines have significantly improved liquidity since March. Rated airlines have sufficient liquidity to survive on average for about 450 days at current low activity levels. For weaker airlines, this may be insufficient if groundings persist into 2021.

We model two scenarios assuming a recovery by 2023 or later years. Most airlines will carry substantially more debt in 2023. Our faster and slower recovery cases assume 2023 passenger volumes recover to around 95% and 85% of 2019 levels, respectively. The airlines we rate will carry on average 20%-30% more debt in 2023 compared with 2019, with leverage on average 0.5x-1.5x higher.

We have downgraded 13 airlines since 25 May 2020, and confirmed six. We placed ratings for 22 airlines on review for downgrade in March. The sufficiency of liquidity, and the potential for individual companies to retire the debt incurred to restore credit metrics through 2023 were key considerations in resolving the reviews.

The industry will undergo substantial permanent structural changes. Potential for failures of weaker airlines and government intervention to leave fewer, larger companies, polarised between more efficient operators and strategic state-supported airlines. Health screening and risks of denied boarding will affect travelers potentially beyond the pandemic. Corporate travel is likely to be impaired into 2023. Governments may require deeper carbon emissions reductions from airlines.

There will be deep repercussions across related sectors, particularlycommercial aerospace manufacturers and suppliers, airports, travel distributors and airline service companies. Providers of jet fuel and aircraft lessors will also be deeply affected. By contrast, carbon dioxide emissions will reduce by 750-900 million tonnes over 2020-21.

Latin America, May 11, 2020 – Sovereigns in Latin America (LatAm) are facing the coronavirus shock with higher debt and interest burdens and less overall fiscal space than they had during the 2015-16 commodity price shock. At the same time, investor risk perceptions toward emerging markets have deteriorated, rendering financing conditions less favorable. LatAm sovereigns will face increased funding challenges this year as they post larger deficits amid higher health-related spending, lower tax revenue intake as economies contract, and countercyclical fiscal measures, which include higher spending and tax payment delays in some cases. With access to the global financial markets affected by higher risk perceptions, persistent volatility and higher crossborder funding costs, sovereigns in the region will likely rely on alternative sources of funding (e.g., multilateral funding, local markets, fiscal buffers) to cover the anticipated increase in their borrowing needs.

» Fiscal metrics will deteriorate across the region as debt and interest burdens rise. We expect LatAm sovereigns to come out of the coronavirus crisis with weaker fiscal metrics. As the region’s economies contract and governments post wider fiscal deficits this year, debt burdens will rise by seven percentage points of GDP on average, with the median LatAm debt burden reaching 54% of GDP. And as debt stocks grow and borrowing costs rise, the median interest-to-revenue ratio in LatAm will increase to 13.7% in 2020 – almost two percentage points higher than in 2019.

» Risk differentiation by investors have led to uneven changes in relative borrowing costs across LatAm compared to prior episodes of financial volatility. Since March, spreads have widened more than in previous episodes of market volatility, including the 2013-14 “taper tantrum” period. But this time around, there is significant risk differentiation between lower rated sovereigns. Although the benchmark US treasury rate has been declining, the average LatAm sovereign’s borrowing costs are almost 200 basis points higher than at the beginning of the year.

» Funding strategies to cover coronavirus response will be influenced by market conditions. Higher yields reflecting increased sovereign credit risk premiums will influence funding mix decisions through the rest of the year. We expect governments to rely more extensively on multilateral financing, local borrowing and other funding sources to cover wider fiscal deficits. Because governments will likely gravitate toward funding mixes that minimize interest costs for borrowings, this can partially mitigate the deterioration we anticipate in debt affordability.

Argentina, April 27, 2020 – Argentina’s aviation agency Administración Nacional de Aviación Civil (Argentina) or ANAC, announced that all commercial air traffic, international and local, will remain restricted until 1 September. The restriction is credit negative for Aeropuertos Argentina 2000 S.A. (AA2000, Caa3 negative) because it will receive no passenger revenue until September and the prolonged restriction comes in the middle of an exchange offer process that AA2000 initiated on 21 April to extend its 2020 debt amortization payments until May 2021. ANAC’s resolution does not mean that there will be no flights through September, but instead flights will be pre-approved by ANAC on a case-by-case basis. We expect flights through September to be very limited. AA2000 is working on several cost-saving measures to preserve its cash position, including lowering capital expenditures to a minimum and suspending all pending construction works, among others, in addition to the additional liquidity relief the company is seeking to obtain through its debt exchange offer. Air traffic in Argentina continued operating normally until mid-March when the transportation ministry suspended all commercial air traffic, in line with government-mandated national movement restrictions in response to coronavirus. Pre-coronavirus AA2000 traffic trends were solid. Total traffic growth in 2019 was at 9% over the previous year, but the company now expects traffic to drop as much as 48% for 2020 (see Exhibit 1).

Sources: AA2000 and Moody’s Investors Service

AA2000 offered to exchange its outstanding $350 million 6.875% senior secured notes due in 2027 for newly issued 6.875% cash/9.375% payment-in-kind (PIK) Class I Series 2020 additional senior secured notes due in 2027. Terms of the Series 2020 additional notes will be largely identical to the existing notes, but the quarterly interest payment originally scheduled to be paid in cash on 1 May 2020 will be paid in cash in the form of an interest premium or by a PIK by increasing the principal amount of the additional notes to be issued on the settlement date. Furthermore, quarterly interest payments originally scheduled to be paid in cash on the existing notes on 1 August and 1 November 2020 and 1 February 2021 will be by PIK at a rate of 9.375% per year (see Exhibits 2 and 3). Quarterly amortization payments originally scheduled for 1 May 2020 through 1 February 2021 will be deferred to begin 1 May 2021 and continue under a new principal amortization schedule until maturity. The Series 2020 additional notes and the existing notes will be secured by the same collateral on a pro rata and pari passu basis in accordance with the Indenture and the related collateral documents. It is a condition of the exchange offer, among others, that at least 80% of the existing notes’ outstanding principal amount is validly tendered for exchange and not withdrawn. The company does not expect to modify the offer terms despite the traffic suspension.

Source: AA2000

AA2000 was incorporated in 1998 after winning the national and international bid for the concession rights for 35 airports that handle more than 90% of Argentina’s arriving and departing passengers and include the three airports that serve the capital city of Buenos Aires – Ezeiza (EZE), Aeroparque (AEP) and Palomar (EPA) Airports.

United States, April 13, 2020 – Incoming data in the US (Aaa stable) is beginning to capture the extent to which the coronavirus shock is likely to weigh on the economy. But this rapidly unfolding recession, particularly the way in which it is impacting the economy, is qualitatively different from past business cycle downturns. Unlike previous economic downturns, this shock has its roots outside the economy. The contraction in economic activity is driven by public health policy measures that are aimed at limiting the scale of human suffering from to the spread of the disease. This has resulted in an almost overnight shutting down of a large number of ways in which individuals engage with one another in the economy. The massive economic consequences are becoming more clear with every incoming data print, particularly with regards to the labor market. Unlike past recessions, where the repercussions to firms’ earnings and to households’ incomes materialized over several quarters, this time around the income and employment shocks are upfront and immediate. The unusual nature of this shock and the damage it is causing to the economy is particularly evident in labor market data. The latest establishment survey shows that in just one month, from February to March, payroll employment was slashed by 701,000. (By comparison, during the last recession, which accelerated after Lehman Brothers collapsed in September 2007, job losses only started to mount in February 2008 and took five consecutive months to reach a similar level of job losses on a cumulative basis.) As a result, the unemployment rate increased to 4.4% in March from 3.5% in February as per the household survey. However, the precipitous rise in new weekly jobless claims since the week of 16 March (after the March establishment and household surveys were completed) shows an unprecedented 16.8 million job losses in a matter of just three weeks. This amounts to a staggering unemployment rate of 14%, from the 4.4% in March. It is very likely that job losses will continue to mount through April as thousands of businesses struggling to keep afloat relieve workers in an attempt to cut costs. However, fiscal support and incentives for businesses to maintain payroll will likely slow the pace of layoffs in coming weeks, 1 April 2020.

Most job losses are in the services sector and are temporary for now. A closer look at these early labor market indicators reveals that a large proportion of the layoffs are temporary, which means that many businesses expect to rehire once demand picks up again (see Exhibit 1). Furthermore, most of the workers facing job losses are in low paying jobs on hourly wages, or engaged in temporary work. We expect that government support to households and businesses would partially mitigate the income and job losses, particularly if the economy restarts and businesses begin to reopen after this brief second quarter pause due to the stay-at-home measures. Although there is a risk of uneven benefit distributions resulting in permanent job losses in some sectors, the economic costs would magnify with a longer lasting shutdown.

Source: Bureau of Labor Statistics

Of the 701,000 payroll job losses in the March establishment survey, 650,000 were in the services sector. And in the services sector, leisure and hospitality were the worst affected as this was the first sector to see a compression in demand (see Exhibit 2 and 3). The wave of job losses since mid-March, which will be captured in the April non-farm payroll data, are likely to show increasing layoffs in other services sectors as well, such as retail and construction.

Source: Bureau of Labor Statistics

Longer-term labor market outcomes will depend on the duration of quarantines and the effectiveness of fiscal and monetary policy measures. With layoffs surging across industries, as many as 20 million individuals could lose their jobs in a matter for weeks. In addition, many are likely to see their hours curtailed. And while most of the job losses have so far been among low paid workers, high paid workers will likely experience pay cuts the longer it takes for the economy to restart.

If stay-at-home measures and other efforts to contain the virus are effective enough to allow for a relaxation of social distancing measures, businesses will likely gradually resume normal operations in the third quarter. Under this scenario, which underpins our growth forecasts, individuals could return to their jobs, especially where layoffs are temporary. However, the pace of rehiring will likely be slow, as the fear of a renewed spread of the coronavirus is bound to linger for some time without a cure or a vaccine. We believe that the significant fiscal and monetary policy stimulus measures will provide a cushion to the economy in the interim period. In particular, measures aimed at limiting the damage to the balance sheets of households and firms would help jump-start the economy once the social distancing restrictions are lifted.

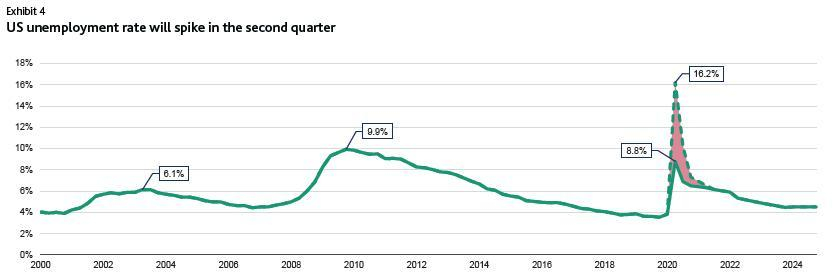

We expect the US unemployment rate to shoot up in the second quarter and to average anywhere between 8.8% and 16.2%, because of the scaling back of work and business closures in response to a sharp pullback in consumer demand (see Exhibit 4). The wide range indicates a significant likelihood of larger layoffs and furloughs in the coming weeks in sectors such as retail, transportation and construction, in addition to hospitality and leisure, which would push the unemployment rate to the high end of the range. In addition, we expect the unemployment rate to peak in the second quarter, and gradually climb down in subsequent months with a gradual resumption of normal economic activity.

We expect some of the job losses to be permanent for two reasons. First, some businesses, particularly small businesses, are unlikely to recover from this shock despite the substantial policy support. As a result, under our baseline forecast, unemployment will average around 6.5% by the end of the year. Our expectation that the unemployment rate will peak in the second quarter is based on the significant fiscal and monetary stimulus measures being undertaken to support the economy (see Exhibit 5). The stimulus will also support households’ purchasing power and aid a gradual resumption of consumer spending in the third and fourth quarters.

There are downside risks to our growth forecasts if the economy remains shut beyond the second quarter. If that were to happen, the unemployment rate will increase further in the third quarter and many of the job losses that we are currently treating as temporary losses will likely become permanent. This would be additionally damaging, not only in terms of household income, but also as a loss of human capital, which takes time to build.

Venezuela, Mar 28, 2020 – Russia-based PJSC Oil Company Rosneft (Rosneft, Baa3 stable), one of the world’s largest integrated oil and gas companies, announced that it had signed an agreement with a company wholly owned by Russia’s government (the name has not been disclosed yet) to sell all of its interest and cease participation in its Venezuelan businesses. The sale includes Rosneft’s five upstream joint ventures, two oilfield services companies and commercial and trading operations. Rosneft will receive a settlement payment equal to a 9.6% stake in Rosneft’s share capital, which Rosneft’s wholly owned subsidiary will hold and will be accounted for as treasury shares. As of 27 March, the market value of the stake was $3.9 billion. The agreement is credit positive for Rosneft because it significantly reduces the risk of further sanctions without materially affecting the company’s asset base and credit metrics. Earlier this year, the US Department of the Treasury’s Office of Foreign Assets Control (OFAC) added Rosneft’s Switzerland-based trading subsidiaries Rosneft Trading SA and TNK Trading International S.A. to its Specially Designated Nationals (SDN) sanctions list, accusing them of breaching US restrictions against trading and transporting oil produced in Venezuela. While the imposed sanctions did not specifically apply to Rosneft itself, despite Rosneft’s stakes in the subsidiaries exceeding 50%, Rosneft’s continuing operations in Venezuela and trading the locally produced oil risked triggering more broad sanctions against the company, potentially undermining its own international sales. Rosneft’s business in Venezuela has been represented primarily by its five upstream joint ventures, which produced 2.2 million tonnes (mt) of oil in 2019 (Rosneft’s share), or less than 1% of the company’s total liquid hydrocarbons (crude oil and gas condensate) production over the same period. In addition, over 2014-17 Rosneft and its associated entities provided around $6.5 billion in prepayments to Venezuelan national oil company Petroleos de Venezuela S.A. (PDVSA) and its joint ventures to purchase their oil and petroleum products for subsequent resale. By 30 September 2019, the latest reporting date at which Rosneft disclosed the outstanding amount of these prepayments, they had declined to around $800 million, or less than 1% of the company’s 2019 revenue.

We do not expect the disposal to have a material effect on Rosneft’s leverage and cash flow metrics because of the small scale of the Venezuelan operations relative to Rosneft’s other businesses, the largest of which is in Russia, where the company produced 98% of its hydrocarbons in 2019. However, Rosneft’s credit metrics will weaken in 2020 because of the drop in oil prices, driven by the global oil oversupply following the collapse of the OPEC+ agreement amid the sharp decline in global economic growth because of the coronavirus outbreak. Assuming the 2020 average oil price at $30 per barrel of Brent and Rosneft’s broadly flat hydrocarbon production volume compared with 2019, we expect the company’s total debt/EBITDA to increase above 3.5x by year-end 2020 from 2.6x a year earlier, and its retained cash flow (RCF)/net debt to decline towards 15% from 23% over the same period (all metrics are Moody’s-adjusted, with Moody’s-adjusted debt including prepayments received for oil deliveries under long-term contracts). Rosneft’s largest shareholders are JSC Rosneftegaz, which is wholly owned by the Russian state and holds an interest of 50% plus one share; BP p.l.c. (A1 stable), which holds 19.75%; and QH Oil Investments LLC, which is controlled by the sovereign wealth fund Qatar Investment Authority and holds 18.93%. The company is listed on the Moscow Exchange and the London Stock Exchange (GDRs), with a free float of around 11%. Should the Russian state’s interest in Rosneft decline as a result of the transaction, we will accordingly assess the effect on Rosneft’s rating and the current high probability of state support to the company in the event of financial distress under our Government-Related Issuers (GRI) rating methodology. That said, we do not expect any changes in the company’s close credit linkages with the Russian government and its status as a strategic holding of the state because of its economic, political and reputational importance to the sovereign.

You must be logged in to post a comment.