Latin America, July 23, 2025 – Latin American sovereign hard currency issuance surged to USD38.6 billion in 1H25, a 54% increase from the previous year and nearly matching the total for all of 2024, Fitch Ratings says in a new report. Ten sovereigns accessed external markets despite global geopolitical volatility and persistent high US policy rates, as emerging market sovereign spreads narrowed since the April ‘Liberation Day’ spike. However, volatility could return after the US tariff pause ends in August.

Issuance continues to be mainly in US dollars (73%), but this proportion is down from 91% in the first half of 2024, reflecting increased regional interest in diversifying currency exposure. Chile and Mexico issued euro bonds and Uruguay debuted Swiss franc bonds, while Panama stayed out of capital markets but raised significant funds via euro and Swiss franc loans. Activity also continued in global local currency-linked bonds (Dominican Republic, Paraguay).

Barbados returned to international markets with bonds featuring the world’s first pandemic clause, following its 2019 bond with natural disaster provisions. Fitch rated the bond in line with the sovereign’s rating, noting that payment deferrals under the clause would not be considered a default.

Distressed emerging-market sovereign spreads have tightened, although market access for some remains a challenge. Ecuador saw the biggest gain after re-electing a market-friendly government and reaffirming its IMF commitments; Argentina also saw narrowing spreads after securing a new IMF program and receiving a large upfront disbursement. Bolivia still faces high yields, rising default risks, and uncertain prospects ahead of elections and a large bond payment in 2026.

Spain, September 15, 2021 – The Spanish government published Royal Decree Law 17/2021, implementing measures to limit the effect of rising wholesale gas prices on consumers’ electricity and gas tariffs. The law follows a government proposal, currently being debated in parliament, to claw back incremental profits that owners of Spanish nuclear, large hydro and large renewables plants would have gained from higher carbon prices under a no-subsidy regime commissioned before October 2003.1

The new law is credit negative for Spain’s unregulated electricity and gas utilities because it introduces a revenue deduction that will weaken utilities’ credit metrics, heightens political risk and diminishes the opportunities for arbitrage for hydropower generation.

Based on current spot gas prices, the new law will incrementally weaken the financial profiles of Enel SpA (Baa1 stable), Iberdrola SA (Baa1 stable), Naturgy Energy Group SA (Baa2 stable) and EDP – Energias de Portual SA (EDP, Baa3 positive). Their ratios of funds from operations (FFO) to net debt would fall by 20-130 basis points, all else equal, in 2021-22 (see exhibit). Endesa SA (Baa1 stable), whose credit quality benefits from being 70%-owned by Enel, would record a 550-600 basis point decline in its FFO/net debt ratio, given Endesa’s larger proportion of earnings coming from Spanish nuclear and hydro generation.

Sources: Moody’s Financial Metrics and Moody’s Investors Service

The new tax does not take into account the level of hedging already implemented by Spanish utilities for their 2021-22 output at power price levels reflecting gas prices below current levels. Assuming the Spanish government does not extend the tax beyond March 2022, the effect of the clawback on FFO/net debt ratios would be more muted in 2023 at 10-40 basis points (excluding Endesa, for which the effect would be closer to 300-350 basis points). In addition, the negative effect of the tax could be more than offset by higher realized power prices in the generation business.

The law is also credit negative for owners of Spanish nuclear, hydro and large merchant renewables plants because there is a risk that the government will extend the tax if gas prices do not come down materially by March 2022. Additionally, the limit on the increase in TUR will have a modestly negative effect on Naturgy’s debt position, and to a lesser extent Endesa’s, because of a resulting working capital deterioration. Sales and EBITDA should continue to reflect a full cost pass-through, however.

Spain’s new measures include a revenue deduction on nuclear, large hydro and renewables plants not benefiting from a specific remuneration scheme. Indexed on Iberian spot gas prices from 16 September 2021 until 31 March 2022, affected power plants will be taxed under a formula reflecting Iberian spot gas prices as long as spot gas prices exceed €20 per megawatt-hour (MWh). Under that formula, 90% of the estimated upside in wholesale power prices attributed to the wholesale gas price increase will be taxed. The government estimates that the total tax collection, which will be used to reduce consumers’ electricity bills, will equal €2.6 billion.

The measure includes a cap on the increase in the protected gas tariff (TUR), limiting the fourth-quarter 2021 TUR to 4.4% instead of 28% if the TUR were to reflect current wholesale gas prices. The law also limits to 15% the next planned TUR tariff revision for the first quarter of 2022. The Spanish government also plans to implement forced auctions, whereby major power generators must auction some baseload power generation in the forward markets to improve liquidity and open the market to new suppliers. However, it is unclear how utilities that have sold in advance their power plants’ output can offer capacity in an auction without breaking existing contracts.

The law also imposes changes to Spain’s water law, implementing monthly discharges for hydropower plants and minimum volumes of water stored in reservoirs each month. This is to avoid unwanted environmental effects on reservoirs’ plant and wildlife. These changes will reduce arbitrage opportunities for hydropower plant operators and likely trim their profitability.

The Spanish government’s new law illustrates the increasing risks of political intervention related to affordability faced by unregulated utilities, and comes at a time when wholesale power and gas prices are rising significantly. Other EU countries are likely watching the Spanish example closely and may consider similar measures given the electricity sector was prone to political intervention 10-15 years ago, when power prices last spiked. Other countries’ inclination to follow Spain’s example will also reflect each government’s desire to signal energy policy stability and predictability in the context of material investments required to decarbonize Europe’s electricity systems.

Endnotes:

1See Proposed profit clawback on nuclear and hydro is credit negative, impact modest, 4 June 2021.

Credit Outlook: 20 September 2021. Pg. 8 Moody’s Investors Service

Chile, September 21, 2020 – Enel Americas S.A. (ENIA, Baa3 positive) announced its board of directors had green lit a process to merge the non-conventional renewable power generation business under Enel Green Power’s (EGP) non-Chilean Latin American assets into the company. The proposed merger would be done through an exchange of shares with its parent company, Enel S.P.A. (Baa2 positive). If concluded as so, it would be credit positive for ENIA because it would add new dividend streams to support holding company debt with no cash outflow by ENIA or additional debt beyond that of the merged assets themselves. If successful, closing would likely be in second quarter 2021.

Incorporation of EGP’s assets in Argentina (Ca negative), Brazil (Ba2 stable), Colombia (Baa2 stable), Peru (A3 stable), Costa Rica(B2 negative), Guatemala (Ba1 stable), and Panama (Baa1 stable) would add 2.9 gigawatts of solar, wind and hydro power plants already in operation, and another 2.2 gigawatts of installed capacity under execution, constituting a 45% increase over its current installed capacity of 11.3 gigawatts. It would also establish a platform for continued growth of its power generation business aligned to its overall strategy surrounding energy transition, among other strategic objectives. It adds scale, provides further operating and geographic diversification, with solar and wind added to its fuel resource base, and establishes presence in Central America.

The exact financial effects are yet uncertain because financial statements or a summary of the financial condition of the assets are not yet public. However, from a consolidated standpoint, we believe these effects are countered by the likely increase in indebtedness post transaction closing, given the capital requirements for development of these power plants and long-term payback, and the increased representation of cash flows generated in lower rated countries, particularly Brazil.

That being said, holding company debt will likely decrease to less than the 18% reported in June 2020, and additional dividends will add to the $333 million received in 2019, which led to a dividends/interest expense ratio for the holding company of 8.5x and dividends/debt of 34% that year. Additionally, the exchange of shares will increase Enel S.P.A.’s ownership share of the company to above the current 65%, which strengthens the strategic importance of ENIA to its majority shareholder.

Headquartered in Santiago, Chile, ENIA became the successor company of Enersis S.A. after the separation of the group’s Chilean and non-Chilean electricity generation, distribution and transmission assets. Enel Americas holds controlling interest stakes in several regulated utilities and power generation companies operating in Colombia, Peru, Brazil and Argentina. In 2019, the company generated $12.0 billion in Moody’s-adjusted revenue and $4.1 billion in Moody’s-adjusted EBITDA, with a consolidated net adjusted debt to EBITDA of 1.9x and a ratio of cash from operation pre working capital to adjusted debt of 29.6%.

Brazil, September 1, 2020 – the lower house of Brazil’s (Ba2 stable) national congress approved law 6407/2013, also known as the “Natural Gas Bill,” an important step in the modernization of the natural gas industry in the country.

The bill provides an enhanced regulatory and contractual framework that will foster competition and spur up to BRL80 billion in annual investments along the gas supply chain, according to Brazil’s Ministry of Finance (FIRJAN). Natural gas prices will potentially decline around 40% with increased production rates over the next decade, which will lead to lower production costs for electro-intensive industries, a credit positive. The greater availability of natural gas will also contribute to a sustained diversification of Brazil energy matrix as gas-fired thermal power plants become more competitive in future energy auctions. The bill still needs Senate approval for take effect, a process that we expect to conclude within this month.

Approval of the new legislation follows several years of in-depth discussion among regulators and stakeholders, which gained momentum after the government launched the Gas for Growth (Gás para Crescer) program in 2016. The current administration revamped the program in July 2019 and Petroleo Brasileiro SA’s (PETROBRAS, Ba2 stable) asset divestment strategy are gradually reducing market concentration in the production, transmission, storage and distribution of natural gas. The anticipated development growth in offshore pre-salt oil reserves with multiple and independent exploration and production (E&P) companies will double the net supply of natural gas over the next 10 years from the 51 million cubic meters per day in 2019. A significantly larger supply will drive prices lower and reduce the reliance on natural gas sourced from Bolivia (B1 negative).

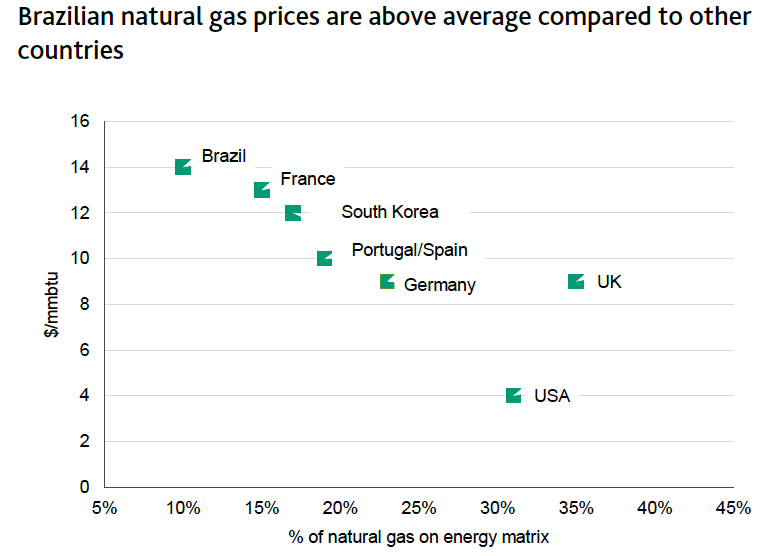

Prices paid by industrial end-users in Brazil have averaged over $14/million British thermal unit (MMBtu), while in Europe the same prices have averaged $7/MMBtu and in the US averaged $4/MMBtu (see Exhibit 1). In the context of possibly lower prices and easier procurement of natural gas, industrial demand will grow. The regulatory changes provide transparency and open access to the natural gas market, which could drive incremental demand growth of around 30% from those industries through 2029, according to Brazil’s energy research company, Empresa de Pesquisa Energética (EPE) (see Exhibit 2).

Exhibit 1

Exhibit 2

Brazil’s energy system will also benefit from greater availability of natural gas through a sustained reduction in prices and improved supply infrastructure. EPE estimates that the current installed capacity of gas-fired thermal power plants in the Brazilian energy matrix can reach 36.2 gigawatts (GW) by 2029, up from 12.9 GW in 2019. Natural gas-fueled thermal power plants can be a reliable alternative to tackle the intermittence of renewable energy generation and replace higher carbon emission sources like coal and oil.

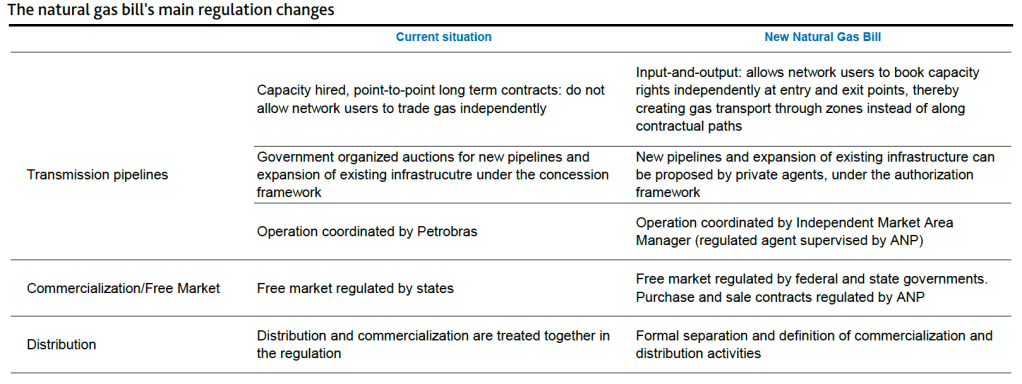

The new legal framework includes provisions to replace the concession system for development of new gas pipelines and commercialization units with an authorization permit procedure, subject to the regulatory oversight of the federal oil agency, Agência Nacional do Petróleo (ANP), which is expected to accelerate the investment rate for end users. It will also ensure open access to the transportation infrastructure (pipelines), which will benefit large industrial consumers of natural gas by allowing for procurement processes that do not depend entirely on the local distribution companies. Nonetheless, the regulation at the state level needs to advance in tandem with federal regulation, clarifying the compensation mechanisms for gas utilities and revenue tax charges (see Exhibit 3).

United States, June 11, 2020 – Eversource Energy (Baa1 stable) announced that it plans to sell 6 million shares of its common stock, which would raise about $517.6 million in gross proceeds based on the previous day’s closing offering price of $86.26 per share. Eversource intends to grant the underwriters a 30-day option to purchase up to an additional 900,000 common shares. Should the full over-allotment be exercised, total proceeds from the offering could reach $595 million.

The planned equity issuance is credit positive because we expect that Eversource will use the net proceeds to pay down outstanding short-term debt, reduce the amount of debt it would have needed to fund future investments and fund a portion of the utility assets acquisition later this year. Consequently, the company’s cash flow coverage metrics will improve.

The equity issuance is part of a plan Eversource announced last year to issue $2.5 billion of equity. It comes as the company increases its capital investment program and acquires utility assets later this year. The company intends to spend $17.3 billion in its core regulated businesses up to 2024, beginning with more than $3 billion last year. The company also plans to invest significantly in clean energy initiatives during this period, particularly offshore wind.

In February, Eversource announced the acquisition of the Massachusetts natural gas assets of Columbia Gas from NiSource Inc. (Baa2 stable) for $1.1 billion. We expect Eversource to finance the transaction with roughly 50% equity and 50% debt. The company expects the transaction to close by the end of the third quarter. The Columbia Gas assets will become a subsidiary of Yankee Gas Energy System, Inc., an Eversource intermediate holding company.

For the 12 months that ended 31 March, Eversource’s ratio of cash flow from operations pre-working capital changes (CFO pre-W/C) to debt was approximately 14.5%, up from 13% in 2018. Eversource’s 2018 financial results were adversely affected by tax reform, as well as $636 million of securitization bonds issued by utility subsidiary Public Service Company of New Hampshire (A3 stable) in May 2018. Including the benefit of the recently announced equity issuance, increased cash flow generation at its utilities and pro forma for the Columbia Gas acquisition, we expect Eversource’s ratio of CFO pre-W/C to debt to improve to about 15% in 2020 and remain in the mid-teens in the coming years.

Headquartered in Hartford, Connecticut, and Boston, Eversource is a utility holding company of mostly regulated utilities including electric, gas and water transmission and distribution companies. With a total rate base of about $19.6 billion, Eversource is the largest utility system in the New England region, serving approximately 4 million electric, natural gas and water customers.

You must be logged in to post a comment.