Brazil, March 24, 2021 – Carrefour S.A. (Baa1 negative) announced the acquisition of Brazilian food retailer Grupo Big S.A. for an enterprise value of around €1.1 billion, equivalent to an estimated 8x enterprise value/EBITDA multiple before synergies. The transaction is expected to close in 2022 following regulatory approval from the Brazilian authorities. Overall, we view the acquisition as credit positive for Carrefour because it will be funded by cash, reducing gross leverage once synergies are achieved, and strengthen its leading position in Brazil.

The acquisition will improve Carrefour’s business profile by increasing its overall scale and geographical diversification, in addition to strengthening its position in Brazil. Carrefour and Grupo BIG are the country’s largest and third-largest food retailers, respectively, and have complementary geographical coverage: Grupo BIG has a strong presence in the north-east and south of Brazil, where Carrefour currently has limited penetration. In addition, the similarity of Grupo BIG’s formats with Carrefour’s (mainly cash and carry and hypermarkets) will facilitate the companies’ integration.

Carrefour will finance the transaction through a mix of cash (70%) and equity (30%) and we expect it to have sufficient cash on balance sheet to fund the acquisition. As a result, Moody’s adjusted debt/EBITDA will decrease by around 0.2x pro forma for the transaction and taking into account around €260 million of run-rate EBITDA synergies that it expects to achieve over a three-year period. However, net debt will deteriorate slightly once the transaction completes because of the estimated €800 million acquisition cost. We also expect restructuring costs to partially offset the additional cash flow from Grupo BIG in the years following the transaction’s closing.

Colombia, January 27, 2021 – Ecopetrol S.A. (Ecopetrol, Baa3 stable) announced the acquisition of 51.4% of the capital of Interconexion Electrica S.A. E.S.P. (ISA, Baa2 stable). ISA is a publicly traded power company owned by the Government of Colombia (Baa2 negative). The transaction is credit positive for Ecopetrol because ISA generates a more stable EBITDA compared to that of Ecopetrol’s oil and gas commodity business, which increases cash flow visibility for Ecopetrol. Also, ISA operates in Colombia, Brazil, Peru and Chile, which reduces Ecopetrol’s geographic concentration risk; and Ecopetrol’s capital structure will not materially change after the completion of the acquisition transaction.

The acquisition of the controlling stake at ISA may cost approximately $4 billion. Because ISA is publicly traded, the acquisition amount should be based on market prices and on standard valuation practices, despite the Colombian government currently controlling Ecopetrol’s and ISA’s capital.

Ecopetrol’s plans to sell shares and assets as well as raise debt to fund the acquisition of ISA. The company expects that the combination of such initiatives will not deteriorate its credit metrics materially. We estimate that Ecopetrol’s debt/EBITDA ratio was around 3 times at year-end 2020 and that this credit metric will remain relatively stable in the next few years, pro-forma for the consolidation of ISA. Our estimate is based on an average Brent oil price of $45 per barrel (dpb) in 2021 and 50 dpb in the medium term.

We understand that after completion of the transaction, ISA will contribute with 15-20% of Ecopetrol’s consolidated EBITDA. We assume that the companies’ business strategies will not change materially and that their respective management teams, dividend policies and capital investment plans will remain mostly unchanged.

Ecopetrol is the largest integrated oil and gas company in Colombia. Ecopetrol has three business segments, namely exploration and production, refining activities and transportation and logistics. Its production averaged around 639,000 barrels of oil equivalent per day, net of royalties, in the 12 months that ended September 2020, and total assets amounted to $43 billion in September 2020. The Colombian government owns 88.5% of the company’s capital and the balance has been traded on the Colombian Securities Exchange since November 2007.

ISA, headquartered in Medellin, Colombia, is an operating holding company with businesses in the electricity transmission, toll roads, telecommunications, and systems management sectors. The company holds direct and indirect ownership stakes in a portfolio of subsidiaries located in Colombia, Brazil, Peru and Chile.

United States, November 18, 2020 – Google parent Alphabet Inc. (Aa2 stable) announced that it will launch Plex Accounts next year, a digital bank account offered within its Google Pay app in partnership with 11 US banks and credit unions. Google’s expansion into the distribution of consumer banking services is credit negative for US banks because it will increase competition for customer relationships, and in particular, competition for deposits, US banks’ primary funding source.

The launch of Google Pay Plex Accounts is an example of big tech’s expansion into retail financial services. It capitalizes on the rising popularity of digital wallets, an example of the widening application of digital innovations in financial services that we expect will continue to drive disruption across banking. Digital innovation and a flourishing financial technology sector present a threat to US banks.

Alphabet’s expansion into retail financial services distribution is consistent with our central scenario that large nonfinancial institutions intent on enhancing customer engagement will partner with incumbent banks to distribute financial services. Alphabet’s ability to partner with US banks and credit unions demonstrates the increasingly low barriers to entry for firms with large existing customer bases to distribute consumer financial services including deposit offerings. Digital innovation and changing customer behavior have lowered such barriers that historically included building out an expensive branch network.

US banks’ balance sheets are built on a foundation of low-cost, sticky deposits. Google Pay Plex Accounts will have no fees for monthly service, low balance, overdraft or in-network ATM use, and market its user-friendly interface and capabilities. Many US banks have similarly introduced online-only deposit products with low to no fees and/or high interest rates to capture additional deposits and customer relationships. Over time, increasing competition could raise deposit costs, pressure deposit fees and increase the need for banks to invest in emerging technology to attract or maintain customers. Failure to respond risks driving shifts in market share to those banks who best meet customer expectations.

The 11 US banks and credit unions partnering with Alphabet to offer Plex Accounts, including Citibank, N.A. (Aa3/Aa3 stable, baa11), would benefit from an inflow of consumer deposits and the potential to deepen new customer relationships. Citibank, N.A. and the other partnering banks will also have an early-adopter advantage in evolving their digital strategies to meet new customer needs. With the accelerating use of mobile payments and rising popularity of single-click digital wallets, incumbent banks need a strategy to stay in the customer-facing part of the payments business.

Alphabet will offer Plex Accounts within its own digital ecosystem, Google Pay, which provides a level playing field for partnering banks. However, the lack of friction within such a digital environment could ultimately increase competition among financial institutions, on and off the platform. Alphabet’s expansion into the distribution of financial services would align with big tech strategies to increase the scope and appeal of their digital platforms through enhanced customer engagement and a further strengthening of their consumer value proposition.

The launch also provides a blueprint for other firms with large existing customer bases keen to capture an increasing share of consumer activity and build customer loyalty. Increased user engagement enables these firms to capture valuable data and boost revenue. In our view, partnerships in which banks cede control of a large share of customer relationships pose the greatest risk to incumbent financial institutions. Such developments increase the risk of our alternate scenario, where big tech firms control a larger share of distribution and displace incumbents that fail to execute timely, effective digital strategies.

Spain, December 3, 2020 – Spain’s lower chamber of parliament passed a 2021 budget, the first budget to be approved since 2018. The bill must still be approved by the upper house before returning to the lower chamber for a final vote, which is expected by the end of the year. However, we anticipate limited amendments. The budget, which targets a general government deficit of 7.7% of GDP for next year, will facilitate the deployment of EU recovery funds key to Spain’s longer-term economic recovery – 2.1% of GDP of which are allocated in 2021 – and introduces several new structural revenue measures.

The budget bill passed at first reading with 188 votes in favour in the 350-seat Parliament. While this strengthens the position of the PSOE-Podemos minority coalition government, the reliance on a constellation of regional parties (nine in total) and the failure to obtain the backing of the centrist Ciudadanos will make it challenging to replicate stable parliamentary support in the future.

In recent years, the lack of a majority government and increased political fragmentation have prevented the passing of a budget and hindered the implementation of reforms to address Spain’s structural challenges. Hence, in 2019 and 2020, the government has had to operate on the previous administration’s 2018 budget after having been unable to find sufficient parliamentary support for a budget of its own. Before that, both the 2017 and 2018 budgets had only been adopted in the middle of the year. Under the Spanish budgetary provisions, the government can roll over the budget and is able to approve revenue and spending measures through decree. However, new taxes require parliamentary approval, and a new budget is a prerequisite to effectively implement the investment projects under the EU recovery funds.

The budget is predicated on relatively optimistic macroeconomic assumptions, with growth expected to rebound strongly in 2021 after this year’s coronavirus-induced shock – reaching 7.2% when excluding the impact of EU funds, and 9.8% when they are included. We project a more modest recovery of 6% (European Commission: 5.4%; IMF: 7.2%) after a projected contraction of 11.4% this year, given the large degree of uncertainty surrounding the recovery path across Europe and the global economy. In addition, we project uneven improvements across sectors – particularly tourism and high-contact services, important ones for Spain – as pandemic worries persist. Given our weaker growth outlook, we also forecast a more moderate narrowing in the budget deficit next year than the government’s expectation, to 8.6% of GDP as many of the pandemic-related support measures tail off and revenues start to recover.

The successful absorption of EU funds will be key to Spain’s longer-term recovery. The budget accounts for the use of around €26.6 billion (2.1% of GDP) in grants next year to strengthen investment, the largest part of which will be directed at projects relating to the green energy transition and digitalisation. The government estimates that the usage of the funds will add 2.6 percentage points to growth annually between 2021 and 2023, but much will depend on their effective implementation. While Spain is well placed to take advantage of the “green transformation” part of the EU’s recovery fund, the needed coordination between the central government and the regional administrations – an inevitability given Spain’s very decentralised system of government – is likely to be one of the main challenges to the funds’ execution. Also key will be the ability to allocate the funds toward high-quality investment projects that raise future productivity and potential growth.

Regarding the outlook for public finances, the 2021 budget includes a series of measures on revenues and spending. New structural revenue measures mark a step toward broadening Spain’s tax revenue base, one of the lowest across large euro area economies (35.4% of GDP in 2019, more than six percentage points below the euro area average of 41.6% of GDP). The measures, which include new taxes on digital companies and financial transactions as well as new steps to fight against tax fraud, are projected by the fiscal council AIReF to yield additional revenues of around €4 billion per year, equivalent to 0.3% of GDP. We expect any future consolidation to come largely through the revenue side given the political orientation of the coalition parties.

Sources: Eurostat, Moody’s Investors Service

Sources: Intervencion General de la Admin del Estado.

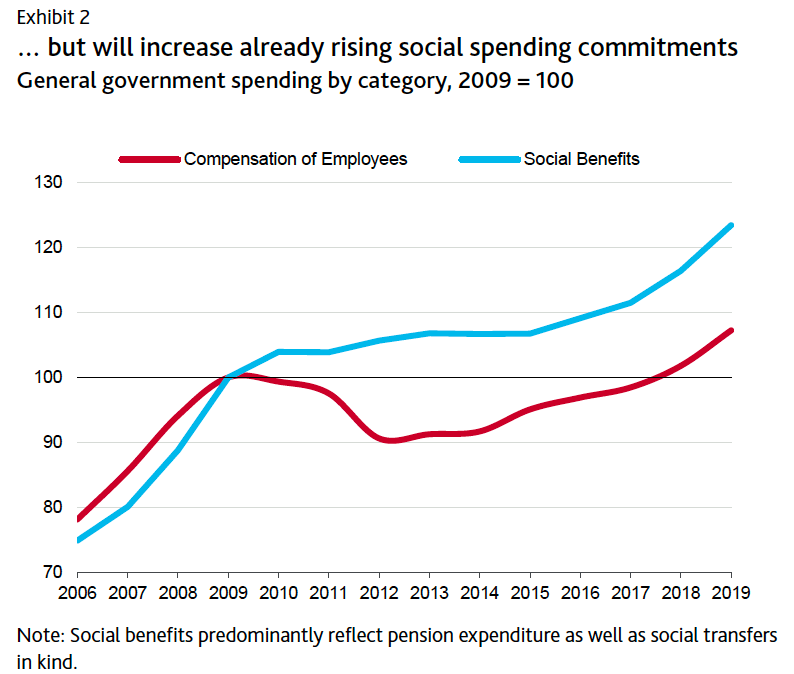

On the spending side, the budget will again increase social spending commitments, in particular through the relinking of pensions to inflation and higher public-sector wages. The public sector wage bill (around a quarter of total general government spending) and social benefits have increased strongly in recent years, in part reversing the consolidation efforts made in the aftermath of the global financial crisis and reducing budget flexibility. The budget also reflects the full-year impact of the new nationwide minimum income scheme, which will cost 0.2% of GDP.

Restoring the public finances to their 2019 level will be a protracted process. We expect Spain’s public debt ratio to rise above 120% of GDP by the end of 2021, an increase of around 25 percentage points from 2019, above the average across the largest advanced economies. Under our baseline assumptions, Spain’s public debt ratio will only stabilise near that level in the following years, leaving the country’s public debt among the highest in the world. That said, the very favourable funding environment and improvements in debt affordability will remain an important mitigating factor for the large increase in Spain’s debt burden.

Despite this year’s much higher issuance of government bonds, the government’s debt interest burden continues to decline as costlier debt is refinanced at lower rates; as of December, the average interest rate on the central government’s debt was 1.86% (from 3.11% in 2015) versus an average cost at issuance of just 0.21%.

Chile, September 21, 2020 – Enel Americas S.A. (ENIA, Baa3 positive) announced its board of directors had green lit a process to merge the non-conventional renewable power generation business under Enel Green Power’s (EGP) non-Chilean Latin American assets into the company. The proposed merger would be done through an exchange of shares with its parent company, Enel S.P.A. (Baa2 positive). If concluded as so, it would be credit positive for ENIA because it would add new dividend streams to support holding company debt with no cash outflow by ENIA or additional debt beyond that of the merged assets themselves. If successful, closing would likely be in second quarter 2021.

Incorporation of EGP’s assets in Argentina (Ca negative), Brazil (Ba2 stable), Colombia (Baa2 stable), Peru (A3 stable), Costa Rica(B2 negative), Guatemala (Ba1 stable), and Panama (Baa1 stable) would add 2.9 gigawatts of solar, wind and hydro power plants already in operation, and another 2.2 gigawatts of installed capacity under execution, constituting a 45% increase over its current installed capacity of 11.3 gigawatts. It would also establish a platform for continued growth of its power generation business aligned to its overall strategy surrounding energy transition, among other strategic objectives. It adds scale, provides further operating and geographic diversification, with solar and wind added to its fuel resource base, and establishes presence in Central America.

The exact financial effects are yet uncertain because financial statements or a summary of the financial condition of the assets are not yet public. However, from a consolidated standpoint, we believe these effects are countered by the likely increase in indebtedness post transaction closing, given the capital requirements for development of these power plants and long-term payback, and the increased representation of cash flows generated in lower rated countries, particularly Brazil.

That being said, holding company debt will likely decrease to less than the 18% reported in June 2020, and additional dividends will add to the $333 million received in 2019, which led to a dividends/interest expense ratio for the holding company of 8.5x and dividends/debt of 34% that year. Additionally, the exchange of shares will increase Enel S.P.A.’s ownership share of the company to above the current 65%, which strengthens the strategic importance of ENIA to its majority shareholder.

Headquartered in Santiago, Chile, ENIA became the successor company of Enersis S.A. after the separation of the group’s Chilean and non-Chilean electricity generation, distribution and transmission assets. Enel Americas holds controlling interest stakes in several regulated utilities and power generation companies operating in Colombia, Peru, Brazil and Argentina. In 2019, the company generated $12.0 billion in Moody’s-adjusted revenue and $4.1 billion in Moody’s-adjusted EBITDA, with a consolidated net adjusted debt to EBITDA of 1.9x and a ratio of cash from operation pre working capital to adjusted debt of 29.6%.

You must be logged in to post a comment.